Assessment process for UBS’s resolvability

Resolvability means creating the conditions for successfully restructuring a systemically important bank in a crisis, or allowing it to exit the market by way of bankruptcy, without jeopardising financial stability. The resolvability of global systemically important banks (UBS in Switzerland) is assessed in accordance with international standards. The following processes are used for this purpose:

- The FSB’s Resolvability Assessment Process (RAP)

- The FINMA resolvability assessment

- Operationalising the resolution plan

The current assessment of the resolvability of UBS is published on a regular basis

The FSB Resolvability Assessment Process

As the main international forum, the Financial Stability Board (FSB) has established the Resolvability Assessment Process (RAP) under which the competent national authorities in the FSB member states assess the resolvability of their G-SIBs every year. FINMA carries out this resolvability assessment in consultation with the most important host supervisory authorities for UBS as a Swiss G-SIB. FINMA reports annually to the FSB chair on the progress made over the previous year and the remaining obstacles to achieving resolvability. Based on these reports, the FSB produces a summary of the resolvability status of all G-SIBs.

The FINMA resolvability assessment

The Swiss too-big-to-fail legislation contained an incentive system under which UBS and the former Credit Suisse were eligible for rebates on their gone concern capital requirements in return for improvements to their global resolvability. These rebates were only granted on the gone concern requirements for the group and parent company and had no impact on the gone concern requirements of the Swiss entity.

Between 2016 and 2022 FINMA evaluated the eligibility of the large banks for rebates every year on the basis of the measures they had implemented. Only measures that went beyond the statutory minimum requirements were eligible for a rebate. Both large banks attained the maximum rebate available under the Capital Adequacy Ordinance.

The rebate system was replaced by the resolvability assessment on 1 January 2023 to continue to set incentives to maintain and improve resolvability. If there are obstacles to resolvability that the bank is unable to eliminate itself within the deadline, FINMA may impose surcharges on the gone concern or liquidity requirements. FINMA will continue to conduct the resolvability assessment for UBS on an annual basis.

FINMA is required to consult the SNB during its evaluation. It can also consult foreign supervisory and resolution authorities.

Assessment of resolvability in the global resolution plan

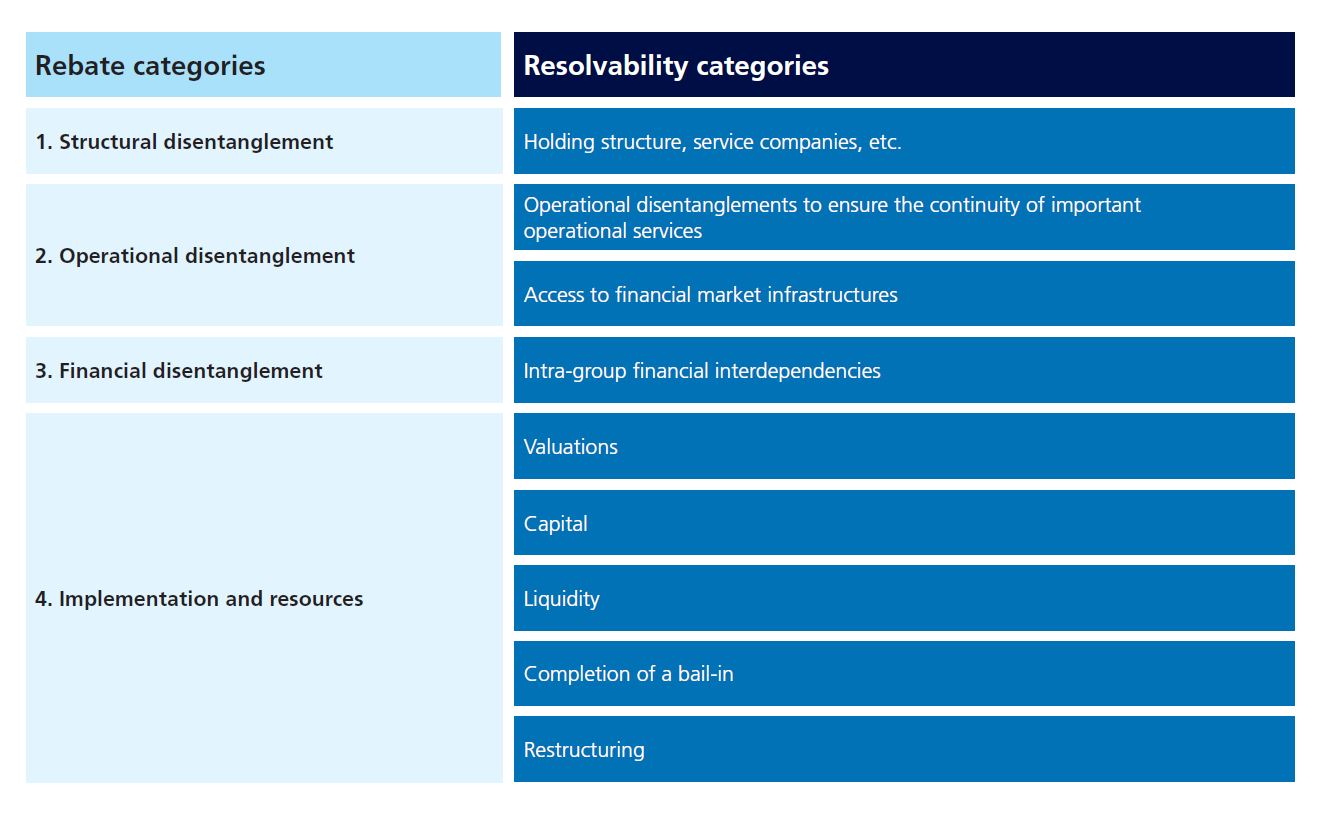

The global resolution plan sets out how FINMA would carry out the restructuring or wind-down of a bank if circumstances required. When assessing the resolvability of UBS, FINMA considers whether the bank has made the necessary preparations to ensure the successful implementation of the plan. For this purpose it has broken down the key requirements into four topic areas based on the international standards drawn up by the Financial Stability Board (FSB).

The first three areas relate to the disentanglement of interdependencies within the group as well as the reduction of external interdependencies, e.g. in relation to financial market infrastructures. The group as a whole and the individual entities within it should not be put at risk by the failure of an individual subsidiary or third party. The fourth area focuses on the question of the operational capabilities the bank must possess in order to adequately support FINMA’s resolution plan.

The current state of affairs with regard to resolvability in the context of the global resolution plan can be found in the Resolution report.