FINMA supervises the Swiss financial centre with the aim of ensuring the stability of the financial markets and protecting investors, creditors and insured persons. In this article, Thomas Hirschi, head of banking supervision, discusses how FINMA uses its proportional and risk-based approach to ensure effective supervision and at the same time relieves the burden on supervised institutions where appropriate and possible.

With its disproportionately large and competitive financial industry, Switzerland is dependent on maintaining a good reputation as a financial centre and constantly renewing it.

FINMA as an independent and integrated supervisory authority has a central role to play here. Its statutory mandate is to ensure the proper functioning of the financial markets and to protect the clients of financial service providers. FINMA’s effective and efficient supervisory activities create the conditions for clients to be able to utilise the services offered by financial service providers in Switzerland with a high level of certainty and for trust in market participants to develop. The supervised institutions themselves also benefit from financial market supervision, as they can conduct their business in a stable environment built on high levels of trust. The benefits that market participants, their clients and the financial centre as a whole derive from supervision must of course always be greater than the costs incurred by supervision.

Proportional and risk-based supervision as an effective approach

FINMA ensures this positive cost-benefit ratio through numerous measures. It organises its supervision to be as proportionate and risk-based as possible and is also committed to proportionality in regulation. It takes into account the size and importance of the respective financial institution, as well as the business model, the respective control environment and the resulting risks. The larger the institution and the more relevant the corresponding risks, the stricter the supervisory expectations and the closer FINMA’s supervision. The reverse is also true: The smaller the institution and the lower the risks, the greater the relief. This proportional and risk-based approach ensures a differentiated and efficient procedure on the part of FINMA and at the same time allows appropriate relief for smaller financial institutions.

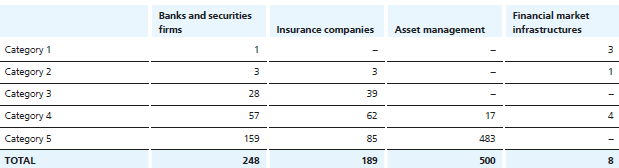

For this purpose, the supervised financial market participants are divided into five categories based on their size and risk potential for investors, creditors and insured persons as well as for the financial centre as a whole. Category 1 comprises the largest and most heavily supervised institutions, while category 5 comprises the smallest and least heavily supervised institutions.

Supervisory categories 2023

Number of supervised institutions in categories 1 to 5

In addition to this categorisation, each institution receives an internal FINMA rating that reflects FINMA’s risk assessment. The supervisory category and the rating determine the intensity of supervision.

Intensity of supervision

Proportionality using the example of banks and securities firms

If we take the regulation of banks as an example, Category 1 and 2 institutions have to fulfil significantly higher requirements in terms of capital, liquidity and risk management. This reflects their categorisation as systemically important, their complex risk structure and the associated systemic risks. They must hold more capital as a buffer against potential losses and fulfil stricter liquidity requirements in order to have sufficient funds available at all times. Larger banks are also obliged to implement stricter corporate governance requirements. Institutions in Categories 1 to 3 must have a risk control and compliance function acting in an independent supervisory capacity. They must also implement further measures to ensure operational resilience, for example against cyber risks, in business continuity management or when handling critical data. In connection with climate risks, systemically important institutions (Categories 1 and 2) must describe the major financial risks and their impact on the business strategy, business model and financial planning. The process for identifying, assessing and mitigating these risks must also be disclosed. Less stringent requirements apply to non-systemically important banks, with a further distinction being made between Categories 3 to 5.

The same applies to supervision. Systemically important institutions (Categories 1 and 2) are subject to ongoing, intensive and close supervision. FINMA uses a wide range of instruments, including regular on-site supervisory reviews, detailed reporting obligations, stress tests and scenario analyses. Category 3 banks are subject to less intensive supervision, while supervision of Category 4 and 5 banks is predominantly data-based. However, an in-depth review is carried out in the event of breaches of regulations or particular irregularities. Reporting is less extensive and there are fewer on-site supervisory reviews.

Specifically, a total of 52 on-site supervisory reviews were carried out at around 220 banks in Supervisory Categories 4 and 5 between 2021 and 2023. In the same period, 116 on-site supervisory reviews were carried out at Category 1 institutions. As a direct result of the on-site supervisory reviews carried out in 2023, FINMA also imposed additional capital requirements on certain institutions. In terms of enforcement activities, in the last ten years FINMA has carried out 20% of its investigations and enforcement proceedings at banks in Categories 1 and 2, even though they account for only 2% of supervised institutions.

On-site supervisory reviews: banks

Average number of on-site supervisory reviews per institution in the banking sector

Successful small banks regime to relieve the burden on small financial market participants

Another example of proportionality is the small banks regime. It has been in force since 2020 and is the only one of its kind in the world. Well-capitalised and well-managed banks and securities firms in Categories 4 and 5 can participate in the small banks regime on a voluntary basis. If they fulfil the relevant criteria, they benefit from simplified regulatory requirements for capital and liquidity. This means that they have to carry out fewer complex calculations to fulfil their capital requirements and they have more flexibility in managing their liquid assets.

At the end of 2023, 54 small banks and securities firms were participating in the small banks regime. This corresponds to a quarter of the supervised institutions in Categories 4 and 5. It provides them with significant relief and a reduced regulatory and supervisory burden.

With the entry into force of the revised Insurance Supervision Act (ISA) and the revised Insurance Supervision Ordinance (ISO), and motivated by the success of the small banks regime, FINMA introduced a small insurers regime for insurance companies at the beginning of 2024. This means that small, well-capitalised, liquid and well-managed insurers in this sector can also benefit from regulatory and supervisory relief.

The limits of proportionality

Proportionality cannot be applied to the same extent everywhere. Although proportionate regulation and supervision means that small institutions do not need to do as much as big players, they still have to identify and limit their risks and ensure that deposits are protected. In particular, FINMA does not grant any relief in the conduct areas of money laundering, investor protection, market conduct and cross-border services.

Small institutions must also implement the regulations on combating money laundering and risk management when offering financial services abroad in order not to jeopardise the reputation of the financial centre. Another example is how sanctions are dealt with, which is the same for all institutions, regardless of their size. Nor can the protection of customers when marketing financial services or carrying out securities orders be counterbalanced against a firm’s capital or liquidity. By their very nature, these risks do not depend on the size of a financial market participant and the corresponding regulations are implemented equally for all supervisory categories.

The future development of proportionality

FINMA is pursuing further initiatives to ensure that supervision and regulation in its area of responsibility are as proportionate as possible and is also committed to a proportional approach in overarching regulation, for example in the finalisation of Basel III and the associated FINMA circulars. In the future, it will continue to examine possible relief when drafting new or updating existing regulations and supervisory approaches and – where appropriate – implement them within the ambit of its statutory mandate.