Real estate market remains tight 2013

In summer 2012, the Swiss Bankers Association (SBA) supplemented its self-regulatory regime for granting mortgages. Anyone wishing to buy a property must now supply at least 10% of the lending value in the form of hard equity not drawn from pension entitlements. Additionally, the loan-to-value ratio is to be reduced to two thirds within 20 years. The aim is to prevent mortgage lenders incurring losses in the event of a moderate drop in property prices and buyers making excessive inroads into their pension entitlements. FINMA approved the SBA’s new minimum requirements for mortgage financing as a supervisory minimum standard.

Moreover, the Federal Council introduced the countercyclical capital buffer in February 2013. As of 1 September 2013, banks are required to hold additional core capital amounting to 1% of their risk-weighted mortgages on Swiss residential properties.

Modest slowdown at a high level

Under the influence of the self-regulatory measures, the countercyclical capital buffer and a slight rise in general long-term interest rates, growth in mortgage volumes fell marginally to below 5% by the middle of the year. However, this is still significantly above the growth in gross domestic product (GDP).

Risks accumulating due to slow amortisation

In the current low interest rate environment, interest payments and amortisation are largely affordable. However, a normalisation of interest rates can quickly lead to financial sustainability squeezes and loan defaults. Unless adequate countermeasures are adopted, the later the upward correction in interest rates, the greater the accumulated risks will be.

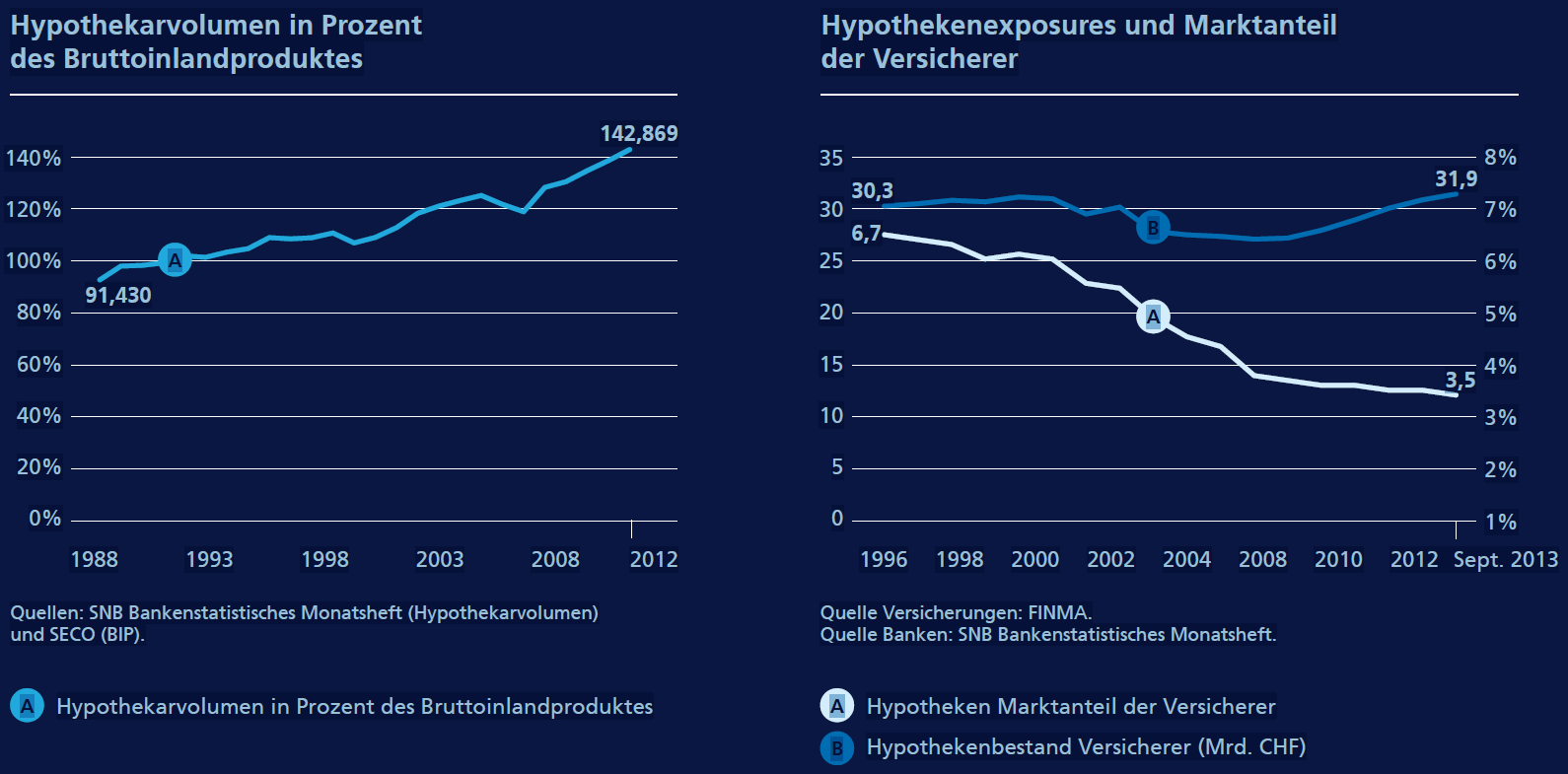

A further aggravating factor is that owing to tax incentives, mortgages are only being amortised slowly despite low interest rates. At 140% of GDP, mortgage debt in Switzerland has now reached a very high level by international standards. Set against this high figure are assets that are often illiquid and are therefore only available to a limited extent to pay down mortgage debt in the short term. More systematic amortisation is therefore a desirable objective.

Dangers of a high vacancy rate

There are also particular risks attached to investment properties, given the historically low gross initial yields. Financial sustainability could be rapidly jeopardised not only if interest rates rose but also if there were high vacancy rates.

Increased inspections by FINMA

FINMA responded to the increasingly acute risk situation by carrying out supervisory reviews and stress tests specifically focused on the mortgage market. This involved stimulating the impact of a rapid rise in interest rates on income and equity capital based on the assumption of a decline in real estate prices coinciding with a deterioration in the economic environment.

Supervisory reviews were carried out at six banks. To obtain a precise picture of mortgage lending, FINMA focused not only on the financing of owner-occupied properties but also on residential investment properties.

Swiss insurers in the real estate and mortgage market

FINMA follows closely Swiss insurers’ exposure to the country’s real estate market, carrying out halfyearly monitoring of their mortgage and real estate portfolios.

Insurers account for less than 4% of the Swiss mortgage market, and mortgages on average add up to just 6% of their capital investments – far less than the 1996 figure of 10%. The loan-to-value ratio of these mortgages averages 52% (gross, excluding collateral), significantly below the limit set by FINMA. Over 90% of mortgages held by insurers are firstrank, more than 31% include additional collateral, and in excess of 32% are amortised. Faced with low interest rates, customers are demanding fixedrate mortgages, and more than 90% of mortgages granted by insurers fall into this category, with an average remaining term of four to five years.

In 2013, insurance companies held real estate valued at CHF 50.5 billion directly in their portfolios, mostly consisting of investment properties. This figure has grown in recent years. In relative terms, however, the proportion of directly held real estate in insurers’ total capital investments has fallen slightly over the last five years, and now stands at an average of 11.2% for life insurers and 6% for non-life insurers. When making direct investments in the real estate market, insurers are required to comply with FINMA rules on property types and valuations.

Trends in the Swiss real estate and mortgage market

(From the Annual Report 2013)